Iowa Moves to Give Medical Cannabis Operators State Tax Relief Under HSB 687

By Jason Karimi | WeedPress

March 6, 2026

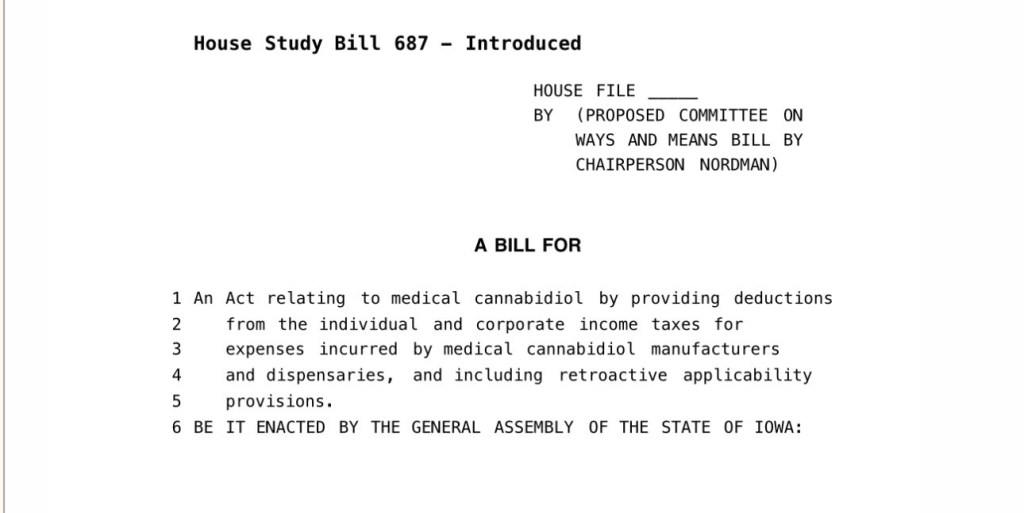

Iowa lawmakers have introduced House Study Bill 687, a tax measure that would let licensed medical cannabis manufacturers and dispensaries deduct ordinary business expenses on their Iowa tax returns even though those same deductions remain blocked at the federal level under Internal Revenue Code section 280E. As of March 4, 2026, the bill was scheduled for a Ways and Means subcommittee meeting on March 10, 2026 at 12:30 p.m. in Room 304.

That may sound technical, but the policy point is simple: Iowa already licenses and regulates these businesses under state law, yet its tax system still piggybacks off a federal rule written to punish trafficking in Schedule I and II substances. HSB 687 would partially break that link at the state level by allowing Iowa-licensed medical cannabis operators to subtract qualifying business expenses “without regard to section 280E of the Internal Revenue Code” for both individual and corporate income tax purposes.

The bill is narrow. It does not legalize broader cannabis commerce, and it does not undo federal tax treatment. What it does is carve out state tax relief for entities licensed under Iowa Code chapter 124E. The text also says the deduction would not apply where no properly licensed entity incurred the expense, or where the expense was incurred in violation of Iowa’s prohibited-acts law and was not otherwise authorized by law.

HSB 687 also includes retroactive applicability to January 1, 2026, for tax years beginning on or after that date. That matters because it shows the bill is not just symbolic. If enacted, it would affect real tax liability for the current tax year rather than only some distant future period.

This is not coming out of nowhere. Iowa lawmakers considered a similar measure in 2024, House File 2650. The Legislative Services Agency’s fiscal note on that earlier bill explained the basic issue clearly: because Iowa calculates taxable income from federal income calculations, Iowa currently mirrors the federal 280E disallowance, which prevents licensed medical cannabis businesses from taking ordinary business-expense deductions at the state level too.

That earlier fiscal note also gave a sense of scale. It projected that allowing those deductions would reduce Iowa General Fund revenue, with the largest estimated impact hitting in the first fiscal year because of retroactive application, then smaller continuing annual reductions after that. In other words, legislators have already had this issue in front of them before, along with a concrete fiscal framework for what state-level decoupling from 280E might cost.

The bigger significance is doctrinal and political. States like Iowa cannot change federal scheduling on their own, but they can decide whether state-recognized medical cannabis operators should be punished twice: once by federal law, and again by a state tax code that simply inherits the federal penalty. HSB 687 represents a modest but important statement that if the state is going to authorize a medical cannabis market, it should stop treating its own licensees as if they were ordinary criminal enterprises for state tax purposes.

It is also a reminder that cannabis reform is often happening in fragments. One bill may not expand patient access. Another may not change criminal law. Another may not touch scheduling at all. But tax treatment matters. A state can suffocate a regulated program just as effectively through structural burdens as through outright prohibition. Section 280E has long done exactly that, and HSB 687 is one more example of a legislature trying to limit the damage inside its own jurisdiction.

For now, the immediate next step is the March 10 subcommittee meeting. That hearing will show whether Iowa lawmakers are serious about giving licensed medical cannabis businesses a fairer tax posture, or whether this proposal will join the long list of cannabis-adjacent reforms that get acknowledged, discussed, and quietly parked.

Leave a comment